Home Loan Sanction for Embassy Biome Apartments — Banking Partner Guide

Home loan sanction at Embassy Biome Apartments operates through approved banking partner relationships integrated with the sales team workflow.

Home loan sanction at Embassy Biome Apartments operates through approved banking partner relationships integrated with the sales team workflow. Understanding the loan process helps buyers navigate efficiently and structure financing optimally.

The sales team coordinates banking partner introductions across approved lenders typically including HDFC Bank, ICICI Bank, SBI, Axis Bank, and select non-banking financial companies. Each lender operates on different sanction criteria, interest rate structures, processing timelines, and customer service quality. Buyers should engage multiple lenders rather than accepting the first sanction offered. Interest rate differences of 25-50 basis points across lenders translate into significant savings across 15-20 year loan tenures. Bank reputation, customer service quality, prepayment flexibility, and online banking interface quality all vary meaningfully across lenders.

Sanction-in-principle should be secured before EOI commitment. Sanction-in-principle represents the bank's preliminary commitment to lend a specified amount subject to property documentation and final approval. Securing this before EOI means buyers commit only to commercial terms they can actually finance. The sanction-in-principle process requires income documentation (salary slips, IT returns), credit history (CIBIL score above 750 typically optimal), existing debt obligations, and employment verification. NRI buyers face additional documentation including foreign income statements, tax residency certificates, and country-of-residence credit references.

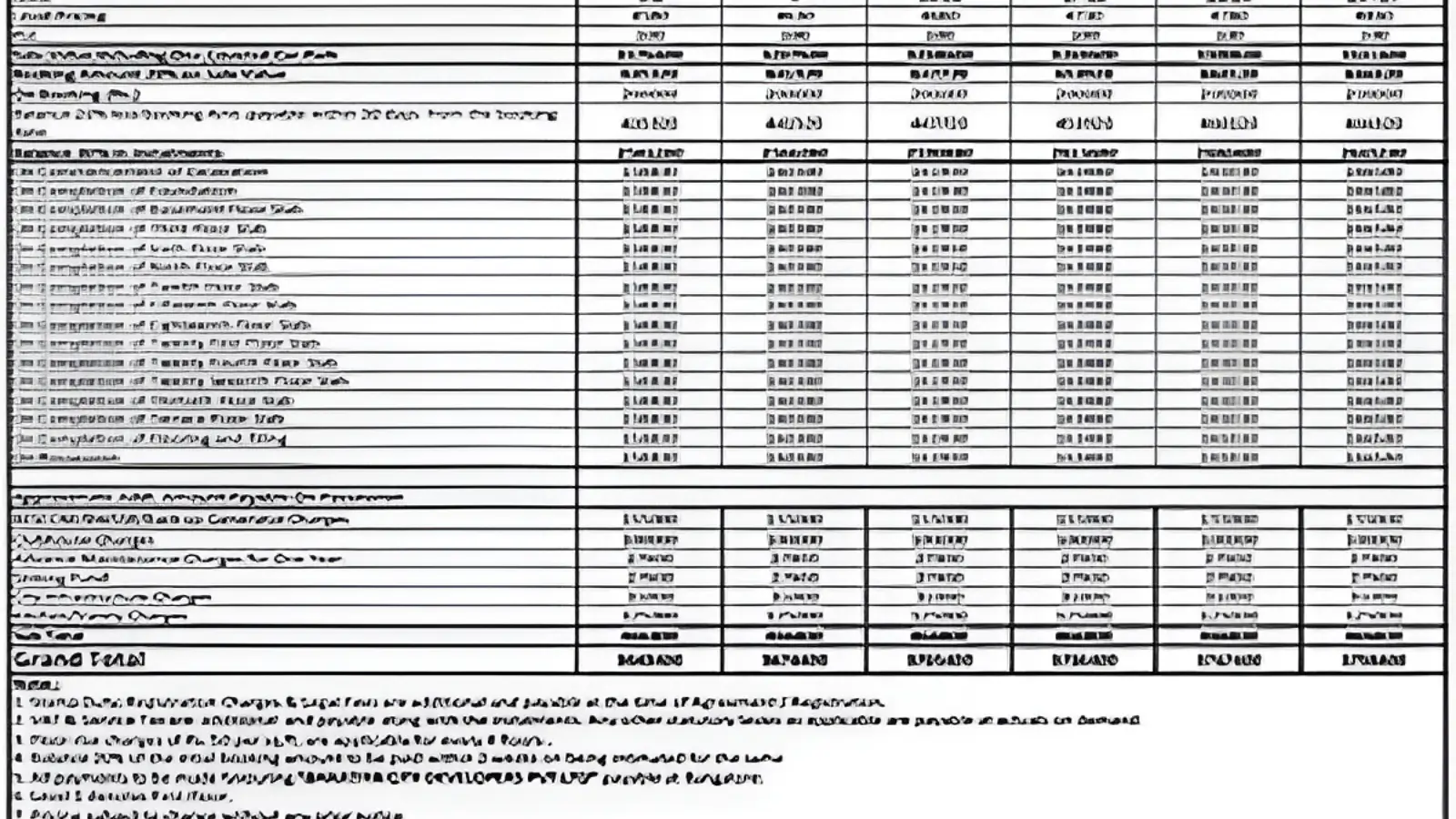

Final sanction approval depends on the specific property documentation. Banks require K-RERA registration, sanctioned plans, allotment letter, agreement-to-sell, and developer NOC for mortgage creation. Embassy Biome's K-RERA registration (in progress) will enable banks to complete property-side diligence quickly upon issuance. Banks typically lend 75-85 percent of property cost depending on borrower profile, with the balance requiring buyer down payment. The 2 BHK at ₹1.60 Cr might secure ₹1.20-1.36 Cr loan amount, requiring ₹24-40 lakh buyer contribution plus statutory taxes and society corpus.

Loan structure choices affect long-cycle financial outcomes meaningfully. Fixed vs floating interest rates differ on stability vs flexibility. Tenure choices (15 vs 20 vs 25 years) affect monthly EMI versus total interest cost. Construction-linked plan loans disburse against milestones, charging interest only on disbursed amounts. Pre-EMI structures defer principal repayment until possession. Prepayment flexibility and partial prepayment policies matter for buyers expecting variable cash flows or potential bonus deployment toward debt reduction. Coordinate the home loan structure with payment plan choice (CLP vs DPP) and individual cash flow situation.

For Embassy Biome Apartment buyers, the home loan workflow should run parallel to the property booking workflow rather than sequentially. Engage banking partners during the diligence phase. Get sanction-in-principle before EOI commitment. Compare loan terms across multiple lenders. Complete loan documentation alongside property documentation. NRI buyers should engage banking partners with strong NRI lending experience for FEMA-compliant workflow integration. The sales team's banking partner integration helps with introductions, but the loan structure decisions sit with the buyer and require independent financial advisory engagement for complex situations or institutional buyer profiles.

Related reading: Airport Corridor Apartments — Why Embassy Biome's Position Matters.

FAQs

What is Home Loan Sanction for Embassy Biome Apartments?

Home loan sanction at Embassy Biome Apartments operates through approved banking partner relationships integrated with the sales team workflow.Why consider Embassy Biome for investment?

Loan structure choices affect long-cycle financial outcomes meaningfully.What makes Embassy Biome distinctive?

The sales team coordinates banking partner introductions across approved lenders typically including HDFC Bank, ICICI Bank, SBI, Axis Bank, and select non-banking financial companies.

Related Articles

Embassy Biome Apartment Cost Sheet — Beyond the EOI Benchmark

EOI pricing at Embassy Biome Apartments anchors at ₹12,000-13,000 per sq.ft. — translating into ticket sizes from ₹1.60 Cr (2 BHK) to ₹2.70 Cr+ (3.5 BHK).

Embassy Biome Apartment Resale Liquidity Analysis

Resale liquidity at Embassy Biome Apartments affects both investment positioning flexibility and long-cycle value defence. Understanding apartment resale.

Embassy Biome Apartment as Yield-and-Appreciation Asset

Embassy Biome Apartments function as yield-and-appreciation asset class within multi-asset portfolios. Understanding the asset class characteristics helps.

Embassy Biome Apartments vs Other Township Apartment Inventory

Apartment components within integrated townships represent the comparison set most directly relevant to Embassy Biome Apartments. Other Bangalore integrated.